This is why specialist beauty retailers companies would open your eyes for investment.

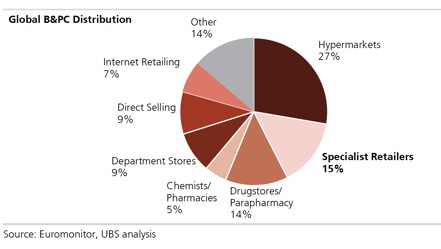

Specialist retailers represent 15-20% of the beauty market and have been gaining share from traditional channels globally.

We partnered with UBS Evidence Lab to identify the winners in this fast-growing channel in the US, UK and Europe (panel data coverage of this channel is patchy, at best).

Our analysis considers 9 million records in 200,000 unique beauty product SKUs from specialist retailer websites (e.g. Ulta, Sephora, Boots), as reported by UBS Evidence Lab in their report Who’s winning with specialist beauty retailers: August edition.

UBS Evidence Lab find that (1) the gap between forerunners L’Oréal and Estée Lauder has been closing in some markets; (2) company trends differ significantly across categories/markets; and (3) smaller brands are outperforming, particularly in skin care.

After a mixed July, L’Oréal’s trends slightly improved across multiple markets, including good performance in US skin & fragrances and in UK/Europe make-up.

Estée has been a strong challenger to L’Oréal YTD but has taken a pause this month in the US.

Coty continues to underwhelm in the US, but it saw improving trends in UK hair and Europe makeup. Other multinationals like P&G, Unilever, Henkel, Beiersdorf are underexposed to this channel, although Unilever and P&G perform strongly in UK hair. Private label underwhelms, except in Europe skin/makeup.

Small brands have gained share in the best-seller lists at the expense of large brands in 60% of the region/category combinations we have analysed.

Their share was up in skin care in all regions, and in makeup in the UK and Europe.

However, larger brands performed better in hair in the UK and Europe, and in fragrances in the US and Europe.

L’Oréal’s lead in specialist retailers is a competitive advantage that supports its +4% volume growth.

Mixed trends need to be tracked closely but we see August’s data as encouraging. Specialist retailer channel is still small for P&G (Buy), Unilever (Neutral), Beiersdorf (Neutral) and Henkel (Sell), but how quickly they build presence might become an increasingly important investment debate.

UBS Evidence Lab harvested beauty product records from c30 retailer websites across 7 countries since October 2015. The database now totals >20m records.

In this version of the report, we focus on the specialist retailers (such as Sephora, Ulta, Boots) in the US, UK and Continental Europe (France, Italy and Germany).

This subset of the data totals 9 million records covering ~200,000 unique SKUs.

Specialist retailers, such as Ulta, Sephora and Boots, make up c15-20% of the $440bn Global Beauty market.

Their share is similar in the US, UK and Continental Europe.

Specialist retailers have increased their share of the Global Beauty market by +100bps from 2009-16.

“We estimate they have averaged +6% growth during this time, outperforming the beauty category growth of +5% (cFX)”,

Business of Fashion, an online publication, conclude that only one third of Estee Lauder’s total growth depends on its own stores.

The brand has opened its own retail stores in many department stores and tourist areas. By contrast, L’Oreal has opted for boosting its own makeup brands.